Markets2026.05.05

Private Credit Just Hit $2.5 Trillion — and Regulators Are Getting Nervous

사모대출 시장이 2.5조 달러를 돌파했어요 — 그리고 규제 당국이 긴장하기 시작했어요

The Shadow Bank Boom

The $2.5 Trillion Market You've Never Heard Of

당신이 들어본 적 없는 2.5조 달러짜리 시장

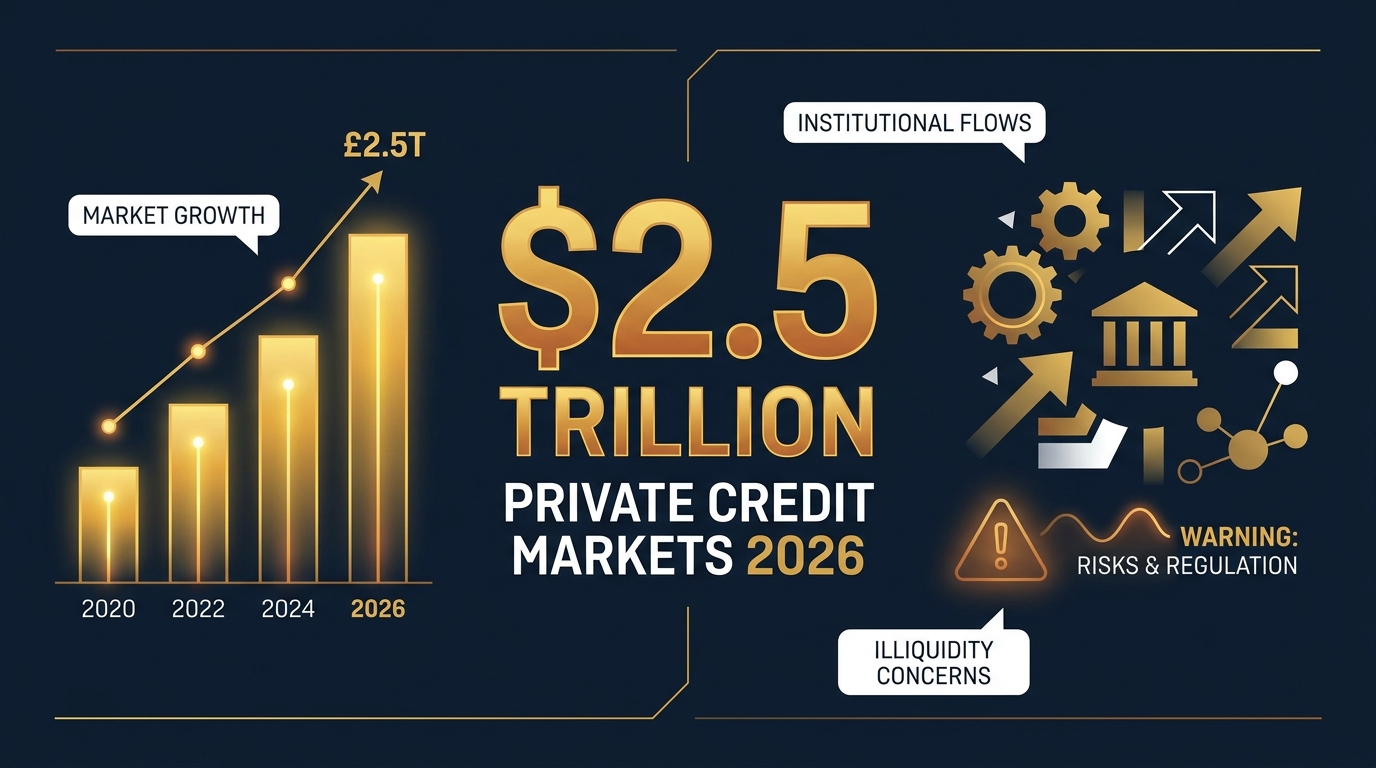

When a company needs a large loan today, it increasingly does not go to a bank. Instead, it turns to private credit funds — private investment firms that lend directly to businesses, bypassing traditional banks entirely and operating largely outside public scrutiny. This market has exploded from $1 trillion in 2020 to $2.5 trillion in assets under management today — and a new warning from global regulators suggests the speed of that growth may be its most dangerous feature.

오늘날 기업이 대규모 대출이 필요할 때, 점점 더 은행을 찾지 않아요. 대신 private credit(사모대출) 펀드를 찾아요. 전통 은행을 완전히 우회하고 대부분 공개적 감시 밖에서 운영되며 기업에 직접 대출을 제공하는 사모 투자회사들이죠. 이 시장은 2020년 1조 달러에서 오늘날 assets under management(운용자산) 기준 2.5조 달러로 폭발적으로 성장했어요. 그리고 글로벌 규제 당국의 새로운 경고는 그 성장 속도 자체가 가장 위험한 특성일 수 있다고 지적해요.

Why Banks Stepped Back

The Regulation That Created a Giant

거인을 만들어 낸 규제

To understand private credit, you have to go back to the 2008 global financial crisis. After the crisis, governments worldwide tightened banking regulations under the Basel III framework — requiring banks to hold more capital against risky loans, which made lending to mid-sized companies and private equity-backed businesses far less attractive. Private credit funds faced none of those constraints: they could lend aggressively, charge higher interest rates than banks, and offer borrowers speed and flexibility that regulated lenders could not match. Institutional investors — pension funds, insurance companies, sovereign wealth funds — poured money in, attracted by returns that typically exceeded public bond markets by three to four percentage points.

사모대출을 이해하려면 2008년 글로벌 금융 위기로 돌아가야 해요. 위기 이후 전 세계 정부는 바젤 III 프레임워크 아래 은행 규제를 강화했어요. 은행들이 위험 대출에 대해 더 많은 자본을 보유하도록 요구했고, 이는 중견기업과 사모펀드 후원 기업에 대한 대출을 훨씬 덜 매력적으로 만들었어요. 사모대출 펀드는 그런 제약을 전혀 받지 않았어요. 공격적으로 대출하고, 은행보다 높은 이자율을 부과하고, 규제를 받는 대출기관이 맞출 수 없는 속도와 유연성을 차입자에게 제공할 수 있었어요. 기관 투자자들, 즉 연기금과 보험사, 국부펀드들이 자금을 쏟아부었어요. 일반적으로 공개 채권 시장보다 3~4%포인트 높은 수익률에 이끌렸기 때문이에요.

The Hidden Risk

The Problem with Loans You Can't See

볼 수 없는 대출의 문제

The Financial Stability Board — the international body that monitors risks across the global financial system — issued a formal warning this week that the private credit boom is creating conditions for a dangerous liquidity shock. The core concern is that, unlike public bond markets, private credit loans are not required to mark to market — meaning they do not have to be repriced daily to reflect changes in borrower health or market conditions. When borrowers struggle, the stress can remain invisible on paper for months — masking a build-up of systemic risk that only becomes apparent when a wave of defaults arrives simultaneously. The FSB's warning echoed concerns that have been building for two years: that as the market grows, so does the potential for a shock — a major recession, a sudden rate spike, or a geopolitical disruption — to trigger cascading failures across thousands of private loans at once.

금융안정위원회(FSB), 즉 글로벌 금융 시스템 전반의 위험을 감시하는 국제기구가 이번 주 사모대출 붐이 위험한 liquidity shock(유동성 충격)을 위한 조건을 만들고 있다는 공식 경고를 발표했어요. 핵심 우려는, 공개 채권 시장과 달리 사모대출은 mark to market(시가평가)이 의무가 아니라는 점이에요. 즉 차입자의 재무 상황이나 시장 상황 변화를 반영해 매일 가격을 재조정할 필요가 없다는 뜻이에요. 차입자들이 어려움을 겪을 때, 그 스트레스는 몇 달 동안 서류상으로 보이지 않는 채로 남아 있을 수 있어요. systemic risk(시스템 리스크)의 축적을 감추고, 대규모 연체가 동시에 발생할 때야 비로소 드러나게 되는 거예요. FSB의 경고는 2년간 쌓여온 우려를 반향했어요. 시장이 성장할수록, 단 하나의 충격, 즉 심각한 경기 침체나 갑작스러운 금리 급등, 지정학적 혼란이 수천 건의 사모대출에 걸쳐 연쇄 부실을 촉발할 가능성도 커진다는 것이에요.

Industry Pushback

The Firms Say They're Safer Than Banks

운용사들은 은행보다 더 안전하다고 말해요

The industry's largest managers — Apollo, Ares, and Blackstone — have pushed back strongly, arguing that their standards are more rigorous than traditional bank lending, not less. They point out that private credit funds lend primarily to established mid-market businesses with real cash flows — not to the speculative borrowers that caused the 2008 crisis — and that their investors accept knowingly, in exchange for higher returns. What both sides agree on is that the market is now large enough that it can no longer be treated as a niche alternative — a $2.5 trillion pool of loans touching thousands of companies worldwide demands a regulatory framework designed for its actual scale.

업계 최대 운용사들인 아폴로, 에어리스, 블랙스톤은 강하게 반박하고 있어요. 자신들의 underwriting(대출 심사) 기준이 전통 은행 대출보다 덜하지 않고 오히려 더 엄격하다고 주장해요. 이들은 사모대출 펀드가 주로 실제 현금 흐름이 있는 확립된 중간 시장 기업에 대출한다고 지적해요. 2008년 위기를 일으킨 투기적 차입자가 아니라는 거예요. 또한 투자자들은 더 높은 수익을 위해 비유동성을 알고 수용한다고 강조해요. 양측이 동의하는 점은, 이 시장이 이제 틈새 대안으로 취급될 수 없을 만큼 커졌다는 것이에요. 전 세계 수천 개 기업과 연결된 2.5조 달러 규모의 대출 풀은 실제 규모에 맞게 설계된 규제 프레임워크를 필요로 해요.

What to watch

Korean Pension Funds Are Deep in This Market

한국 연기금도 이 시장에 깊이 들어와 있어요

The warning matters directly to South Korean savers: the National Pension Service and several other major Korean institutional investors have been steadily increasing their exposure to private credit as part of strategies to boost returns on aging demographic pressures. Watch for any regulatory action requiring private credit funds to report loan-level data to central banks — that disclosure requirement, when it comes, will be the most important structural change in alternative lending since 2008, and it will reshape pricing and access for every borrower in the market.

이 경고는 한국 예금자들과 직결돼요. 국민연금과 다른 주요 한국 기관 투자자들은 고령화 인구 압박에 따른 수익률 향상 전략의 일환으로 사모대출 익스포저를 꾸준히 늘려왔어요. 사모 신용 펀드에게 개별 대출 데이터를 중앙은행에 보고하도록 요구하는 규제 조치를 주시하세요. 그 공시 요건은 2008년 금융위기 이후 대체 대출에서 가장 중요한 구조적 변화가 될 거예요. 여러분이 알아야 할 것은 그 변화가 시장의 모든 차입자를 위한 가격 책정과 접근성을 재편한다는 거예요.