Markets2026.05.02

Profit Under Pressure: What the S&P 500 Correction Is Really Telling Us About Corporate Earnings

수익 압박: S&P 500 조정장이 기업 이익에 대해 말하는 진짜 이야기

Inside a Market Correction

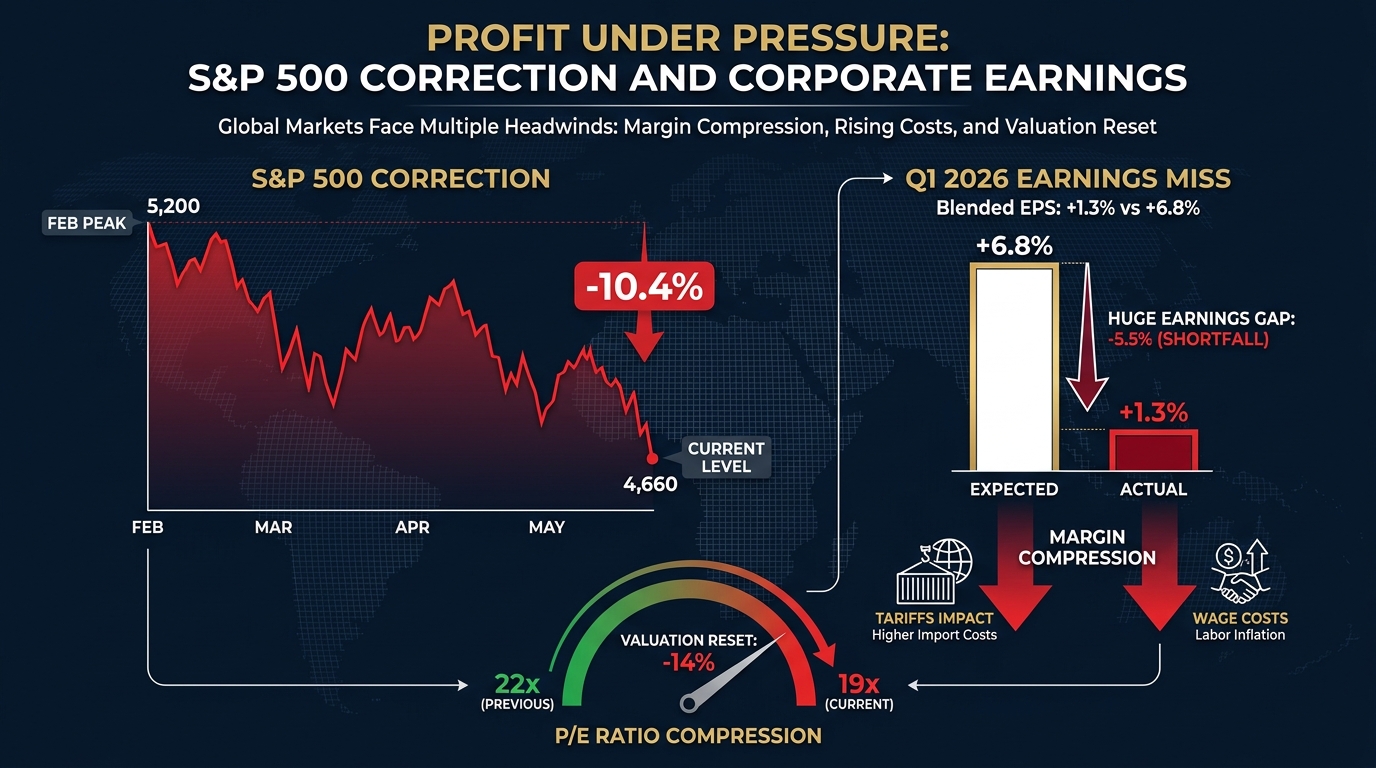

The S&P 500 entered a on Friday — falling more than 10% from its February peak. But the number that really matters is not the index level. It's what companies are reporting inside it. A stock market is defined simply as a decline of 10% or more from a recent peak. It is distinct from a bear market, which requires a 20% drop. Corrections are common — they occur roughly once every year on average — but they are often signals worth decoding, not just price moves to endure.

S&P 500이 금요일 공식적으로 조정(correction) 국면에 진입했습니다. 2월 고점 대비 10% 이상 하락한 것입니다. 그러나 진짜 중요한 숫자는 지수 자체가 아닙니다. 그 안에서 기업들이 발표하는 실적입니다. 주식시장 조정은 최근 고점에서 10% 이상 하락한 것으로 단순히 정의됩니다. 20% 하락을 요구하는 약세장(bear market)과는 구별됩니다. 조정은 흔한 현상입니다. 평균적으로 약 1년에 한 번꼴로 발생합니다. 그러나 조정은 단순히 견뎌야 할 가격 움직임이 아니라, 해독할 가치가 있는 신호인 경우가 많습니다.

The Earnings Miss That Shook Markets

This is being driven by something fundamental: a sharp disappointment in corporate earnings per share (EPS) — the profit a company generates for each share of its stock. With 72% of S&P 500 companies having reported Q1 results, blended EPS growth came in at just 1.3%, far below the 6.8% consensus estimate that analysts had built into stock prices at the start of the year. "Blended EPS" is a term analysts use when some companies in an index have already reported while others have not yet. The "blended" figure combines the actual reported numbers with estimates for the unreported companies, giving a real-time picture of how the earnings season is tracking against expectations. When actual results fall short of the consensus estimate, it is called an earnings miss. When they exceed expectations, it is an earnings beat. This season, the pattern of misses has been unusually broad — across technology, consumer goods, and industrials — rather than concentrated in one sector. That breadth is what is alarming markets.

이번 조정을 이끄는 것은 근본적인 무언가입니다. 기업의 주당순이익(EPS, earnings per share) — 주식 1주당 기업이 창출하는 이익 — 에 대한 날카로운 실망입니다. S&P 500 기업의 72%가 1분기 실적을 발표한 가운데, 블렌디드 EPS 성장률은 겨우 1.3%에 그쳤습니다. 연초 주가에 반영된 애널리스트들의 컨센서스 추정치(consensus estimate) 6.8%를 크게 밑도는 수치입니다. '블렌디드 EPS(blended EPS)'는 지수 내 일부 기업은 이미 실적을 발표했고 다른 기업들은 아직 발표하지 않았을 때 애널리스트들이 사용하는 용어입니다. '블렌디드' 수치는 실제 보고된 숫자와 미보고 기업에 대한 추정치를 결합하여, 어닝 시즌이 예상 대비 얼마나 잘 진행되고 있는지를 실시간으로 보여줍니다. 실제 결과가 컨센서스 추정치에 못 미칠 때 어닝 미스(earnings miss)라고 합니다. 예상을 초과할 때는 어닝 비트(earnings beat)입니다. 이번 시즌에는 한 섹터에 집중되지 않고 기술, 소비재, 산업재 전반에 걸쳐 미스 패턴이 유달리 광범위하게 나타나고 있습니다. 바로 이 광범위함이 시장을 불안하게 만들고 있습니다.

Margins, Multiples, and Double Pressure

The underlying cause is margin compression — a squeeze on corporate profit margins, which measure what fraction of revenue a company actually keeps as profit. For every dollar of revenue S&P 500 companies earned this quarter, they kept less than expected as profit. The culprits are threefold: rising input costs from tariff-driven supply chain disruptions, higher wages in a tight labor market, and slower consumer spending as household savings rates hit a 12-year low. When investors discover that profit margins are being squeezed, they do not just mark down the reported earnings — they also reassess the valuation multiple they are willing to pay for those earnings. The P/E ratio (price-to-earnings ratio) is the most common valuation tool: it divides a company's stock price by its earnings per share. If earnings fall and the multiple investors pay also contracts, the impact on the stock price is doubly painful. This dual pressure — lower earnings plus a lower multiple — is what markets call a P/E re-rating. The S&P 500's forward P/E ratio has compressed from about 22x at the February peak to roughly 19x today. For context: the long-run average is approximately 16x. Even after the , U.S. equities are not historically cheap.

근본 원인은 마진 압박(margin compression)입니다. 기업의 이익률(profit margin) — 매출 중 기업이 실제로 이익으로 남기는 비율 — 이 압착되는 현상입니다. 이번 분기 S&P 500 기업들이 벌어들인 매출 1달러당 이익으로 남긴 비율이 예상보다 낮았습니다. 원인은 세 가지입니다. 관세로 인한 공급망 교란에서 비롯된 투입 비용 상승, 타이트한 노동시장의 임금 상승, 그리고 가계 저축률이 12년 만의 최저치를 기록하면서 나타난 소비 둔화입니다. 투자자들이 이익률이 압박받고 있다는 것을 알게 되면, 보고된 이익을 낮춰 잡을 뿐만 아니라 그 이익에 기꺼이 지불하려는 밸류에이션 배수도 재평가합니다. 주가수익비율(P/E ratio, price-to-earnings ratio)은 가장 일반적인 밸류에이션 도구입니다. 기업의 주가를 주당순이익으로 나눈 것입니다. 이익이 하락하고 투자자가 지불하는 배수도 수축하면, 주가에 미치는 영향은 이중으로 고통스럽습니다. 이 이중 압박 — 낮아진 이익에 낮아진 배수 — 을 시장에서는 P/E 리레이팅(P/E re-rating)이라고 부릅니다. S&P 500의 포워드 P/E는 2월 고점의 약 22배에서 오늘 약 19배로 압축되었습니다. 참고로 장기 평균은 약 16배입니다. 조정 이후에도 미국 주식은 역사적으로 싼 수준이 아닙니다.

Guidance Cuts and Sector Rotation

Adding to the pressure is a shift in forward guidance — the statements companies make about their expected future earnings. Forward guidance is often more important to stock prices than past results, because markets are fundamentally forward-looking machines. This quarter, a record number of S&P 500 companies have issued negative guidance for Q2 and the second half of 2026, citing tariff uncertainty and the prospect of a consumer slowdown. Goldman Sachs cut its year-end S&P 500 target from 5,800 to 5,200 — a meaningful , since major banks' year-end targets are closely watched benchmarks for institutional allocators. Technology and consumer discretionary stocks led the selloff, while energy and utilities outperformed, extending the sector rotation pattern that began last week.

추가적인 압박은 전망 가이던스(forward guidance) — 기업들이 예상 미래 이익에 대해 하는 발표 — 의 변화에서 옵니다. 전망 가이던스는 시장이 본질적으로 미래 지향적인 기계이기 때문에, 과거 실적보다 주가에 더 중요한 경우가 많습니다. 이번 분기에는 S&P 500 기업들 중 기록적인 수가 관세 불확실성과 소비 둔화 가능성을 이유로 2분기와 2026년 하반기에 대한 부정적 가이던스를 발표했습니다. 골드만삭스는 연말 S&P 500 목표치를 5,800에서 5,200으로 낮췄습니다. 주요 은행들의 연말 목표치는 기관 투자자들이 면밀히 주시하는 벤치마크이기 때문에 의미 있는 신호입니다. 기술주와 임의소비재주가 매도세를 이끈 반면, 에너지와 유틸리티는 아웃퍼폼하며 지난주부터 시작된 섹터 로테이션 패턴을 이어갔습니다.

How Corrections Resolve — Or Don't

What does this mean for ordinary investors? A does not automatically become a bear market. Historically, roughly two-thirds of corrections end without crossing the 20% threshold, and the average recovery time from a 10%-15% is about four months. But the key variable is whether corporate earnings — and the guidance behind them — stabilize in the coming weeks. The episode is a reminder of a fundamental principle in equity markets: stock prices are not just a reflection of current earnings, but of expected future earnings discounted back to the present. When those expectations are revised downward simultaneously — as they are now — prices can fall faster than the underlying business performance might suggest. The historical pattern is instructive: in every earnings-driven since 1990, the sectors that led the drawdown were consistently those where analyst consensus had clustered most tightly around a margin-expansion narrative — and in 2026, that narrative is AI productivity gains offsetting rising labor and input costs.

일반 투자자들에게 이것은 무엇을 의미할까요? 조정이 자동으로 약세장이 되는 것은 아닙니다. 역사적으로 조정의 약 3분의 2는 20% 임계치를 넘지 않고 끝나며, 10%-15% 조정에서의 평균 회복 기간은 약 4개월입니다. 그러나 핵심 변수는 기업 이익 — 그리고 그 뒤에 있는 가이던스 — 이 앞으로 몇 주 안에 안정되는지 여부입니다. 이번 사태는 주식시장의 근본 원칙을 상기시켜 줍니다. 주가는 현재 이익만의 반영이 아니라, 예상 미래 이익을 현재로 할인한 것입니다. 그 기대치가 지금처럼 동시에 하향 조정될 때, 주가는 실제 사업 실적이 시사하는 것보다 훨씬 빠르게 하락할 수 있습니다. 역사적 패턴은 교훈적이에요. 1990년 이후 실적 주도 조정마다 하락을 이끈 섹터는 한결같이 분석가 컨센서스가 단일 마진 확장 내러티브 주위에 가장 집중되었던 곳이었어요. 2026년에 그 내러티브는 AI 생산성 향상이 상승하는 인건비와 투입 비용을 상쇄한다는 것이에요.

What to watch

For Korean investors, the S&P 500 carries direct consequences. Samsung Electronics and SK Hynix, major suppliers to U.S. technology companies, are watching whether weaker U.S. tech earnings will translate into reduced orders for memory chips and AI semiconductors. The Kospi index fell in sympathy Friday, led by semiconductor stocks. Watch for guidance revisions, not earnings beats, in this season's reports — when management teams that exceed EPS targets simultaneously lower full-year revenue guidance, that divergence is the most reliable that margin compression is not yet priced into the multiples you are holding.

한국 투자자들에게 S&P 500 조정은 직접적인 결과를 가져옵니다. 미국 기술 기업들의 주요 공급업체인 삼성전자와 SK하이닉스는 미국 테크 기업들의 약한 실적이 메모리 반도체와 AI 반도체 주문 감소로 이어질지를 주시하고 있습니다. 코스피 지수는 금요일 반도체 주식 주도로 동반 하락했습니다. 이번 어닝 시즌에서 실적 상회가 아니라 가이던스 수정을 주시하세요. EPS 목표를 초과 달성한 경영진이 동시에 연간 매출 가이던스를 하향 조정할 때, 그 괴리가 여러분이 보유한 밸류에이션 배수에 마진 압박이 아직 반영되지 않았다는 가장 신뢰할 만한 신호예요.