Markets2026.05.04

Why Long-Term U.S. Interest Rates Are Rising — and What a Bear Steepener Means for You

장기 미국 금리가 오르는 이유 — 베어 스티프너가 당신에게 의미하는 것

The Yield Curve Just Un-Inverted

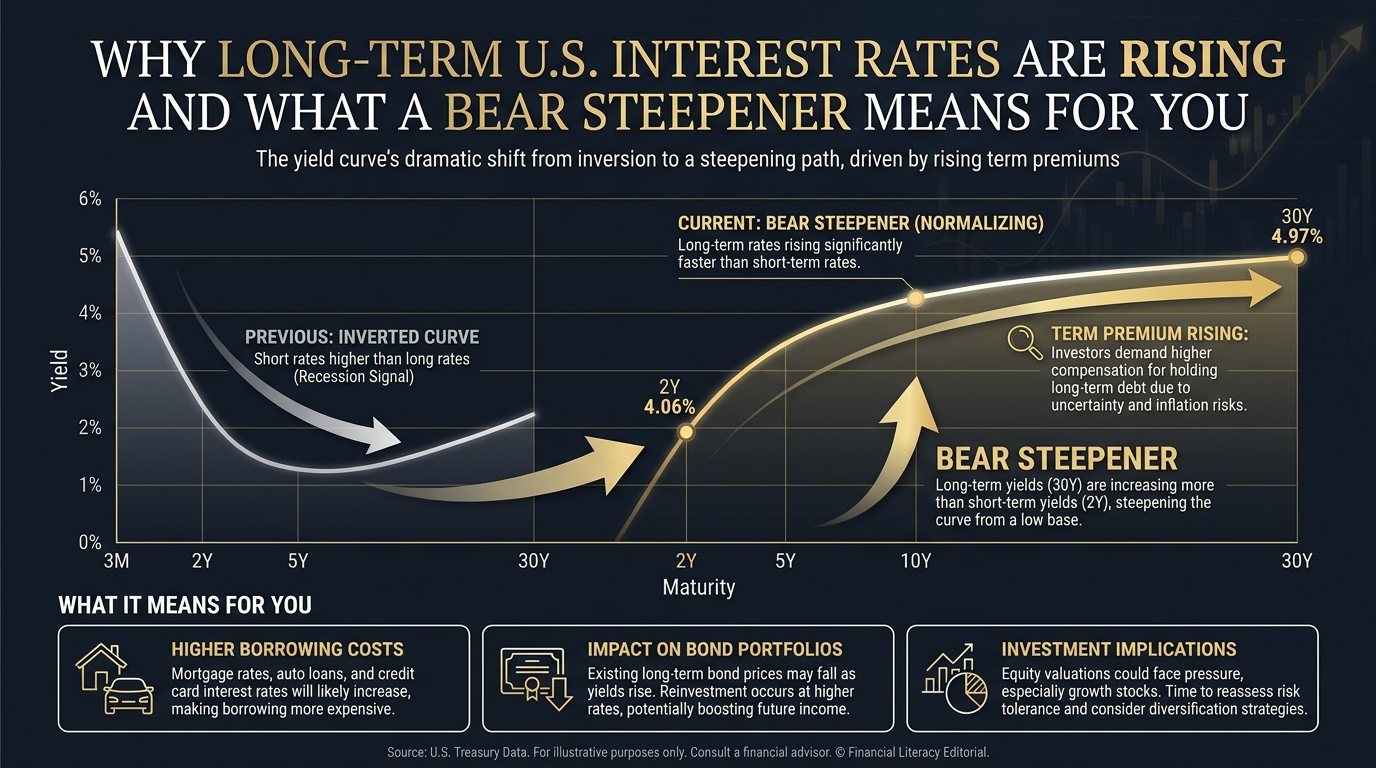

Something important happened in U.S. bond markets this week that most headlines missed. After more than two years, the U.S. Treasury yield curve un-inverted. The 30-year Treasury yield climbed to 4.97%, while the 2-year yield fell to 4.06%, pushing the gap — called the spread — to positive 39 basis points. If those terms are , do not worry: by the end of this article, you will understand exactly what they mean and why they matter for your savings, your investments, and the broader economy. Let us start with the basics. A bond is a loan you make to a government or corporation. In exchange, they pay you a regular interest payment — called a coupon — and return your principal at the end of the loan period, called the maturity date. A yield is simply the effective annual return you receive on a bond, expressed as a percentage. When bond prices fall, yields rise — they move in opposite directions. U.S. Treasury bonds are the government's bonds: the safest debt instruments in the world, backed by the full faith and credit of the United States government.

이번 주 미국 채권시장에서 대부분의 헤드라인이 놓친 중요한 일이 일어났습니다. 2년 넘게 지속된 미국 국채 수익률 곡선(yield curve)의 역전이 해소됐습니다. 30년물 국채 수익률이 4.97%로 상승한 반면, 2년물 수익률은 4.06%로 하락하며 이 격차 — 스프레드(spread)라고 부릅니다 — 가 양수인 39베이시스 포인트(basis points)로 전환됐습니다. 이 용어들이 낯설더라도 걱정하지 마세요. 이 글을 마치면 이 용어들이 정확히 무엇을 의미하는지, 그리고 왜 여러분의 저축, 투자, 그리고 더 넓은 경제에 중요한지 이해하게 될 것입니다. 기본부터 시작해 봅시다. 채권(bond)은 정부나 기업에게 빌려주는 대출입니다. 그 대가로 그들은 쿠폰(coupon)이라고 불리는 정기적인 이자를 지급하고, 대출 기간이 끝나는 만기일(maturity date)에 원금을 돌려줍니다. 수익률(yield)은 채권에서 받는 실질적인 연간 수익률을 백분율로 표현한 것입니다. 채권 가격이 떨어지면 수익률이 오릅니다 — 이 둘은 반대 방향으로 움직입니다. 미국 국채(U.S. Treasury bonds)는 정부의 채권으로, 미국 정부의 완전한 신용으로 보장된 세계에서 가장 안전한 채무 수단입니다.

Reading the Yield Curve

The yield curve is simply a chart showing the yields of Treasury bonds across different maturities — from 1 month to 30 years. Under normal conditions, the yield curve slopes upward: you receive a higher yield for lending money for longer periods, because there is more uncertainty over 30 years than over 3 months. This makes sense: if you lock up your money for decades, you want more compensation for that patience and for the risk that conditions change. A yield curve inversion occurs when this normal pattern flips: short-term yields become higher than long-term yields. This happened in the United States starting in early 2024. The reason: the Federal Reserve had pushed the federal funds rate — the overnight lending rate that anchors short-term yields — to 4.25%–4.50%, while markets expected the Fed to eventually cut rates, which kept long-term yields relatively lower. An inverted yield curve is famous for one thing: it has preceded every U.S. recession in the past 50 years, with a typical lag of 12–18 months. It signals that investors expect short-term rates to fall in the future — usually because they expect a recession to force the Fed to cut.

수익률 곡선(yield curve)은 단순히 1개월에서 30년까지 다양한 만기(maturities)에 걸친 국채 수익률을 보여주는 차트입니다. 정상적인 상황에서 수익률 곡선은 우상향합니다. 3개월보다 30년 동안 불확실성이 더 크기 때문에, 더 오랜 기간 돈을 빌려줄수록 더 높은 수익률을 받게 됩니다. 이는 직관적으로 이해가 됩니다. 수십 년 동안 돈을 묶어두면, 그 인내심과 상황이 변할 수 있는 위험에 대해 더 많은 보상을 원하는 것이 당연합니다. 수익률 곡선 역전(inversion)은 이 정상적인 패턴이 뒤집힐 때 발생합니다. 단기 수익률이 장기 수익률보다 높아지는 현상입니다. 이는 2024년 초부터 미국에서 일어났습니다. 이유는 이렇습니다. 연방준비제도가 단기 수익률의 기준점이 되는 단기 대출금리 — 기준금리(federal funds rate) — 를 4.25%–4.50%로 끌어올렸지만, 시장은 Fed가 결국 금리를 인하할 것으로 예상했고 이로 인해 장기 수익률이 상대적으로 낮게 유지됐습니다. 역전된 수익률 곡선은 한 가지 이유로 유명합니다. 지난 50년간 미국의 모든 경기침체에 선행했으며, 보통 12–18개월의 시차가 있습니다. 이는 투자자들이 미래에 단기금리가 하락할 것으로 예상한다는 신호입니다 — 보통은 경기침체가 Fed의 금리 인하를 강제할 것으로 예상하기 때문입니다.

Bear vs. Bull Steepener

This week's shift is called a steepener: the yield curve became steeper, meaning the gap between long-term and short-term yields widened. But there are two very different types of steepeners, and they carry opposite implications. A bull steepener happens when short-term yields fall faster than long-term yields — typically because the Fed is cutting rates as the economy improves. Investors are optimistic. A bear steepener — what is happening now — occurs when long-term yields rise faster than short-term yields. The "bear" in the name reflects the fact that rising bond yields mean falling bond prices, which is bad for bond investors (bears lose money).

이번 주의 변화는 스티프너(steepener)라고 불립니다. 수익률 곡선이 더 가팔라진 것, 즉 장기 수익률과 단기 수익률의 격차가 벌어진 것입니다. 그런데 스티프너에는 두 가지 매우 다른 유형이 있으며, 각각 반대의 의미를 담고 있습니다. 불 스티프너(bull steepener)는 단기 수익률이 장기 수익률보다 더 빠르게 하락할 때 발생합니다 — 보통 Fed가 경제 개선에 맞춰 금리를 인하하기 때문입니다. 투자자들이 낙관적입니다. 베어 스티프너(bear steepener) — 지금 일어나고 있는 일 — 는 장기 수익률이 단기 수익률보다 더 빠르게 상승할 때 발생합니다. 이름에 '베어(bear)'가 들어간 이유는 채권 수익률 상승이 채권 가격 하락을 의미하고, 이는 채권 투자자들에게 불리하기 때문입니다(베어는 손실을 봅니다).

Term Premium and Fiscal Supply

Why are long-term yields rising now? The key concept is term premium — the extra yield investors demand specifically for accepting duration risk: the risk of committing to hold a bond for a long period, during which many things can go wrong. Inflation might rise. The government might run even larger deficits. The dollar might weaken further. Term premium is essentially the market's insurance charge for long-term uncertainty. For most of 2010–2021, the Federal Reserve's large-scale bond-buying programs — called quantitative easing — artificially suppressed term premium by removing enormous quantities of long-dated Treasury bonds from the market. With QE over and the Fed now shrinking its balance sheet (quantitative tightening), that suppression has lifted. The more immediate driver is the U.S. government's fiscal deficit — the gap between what the government spends and what it collects in taxes — and the sheer volume of new Treasury bonds that deficit requires. The U.S. fiscal deficit is running at 7.2% of GDP in 2026. To fund that gap, the Treasury must issue approximately $2.1 trillion in net new bonds this year. That is an enormous increase in bond supply. Basic supply and demand: when the supply of a product rises while demand stays flat, the price falls. For bonds, lower prices mean higher yields. The market is demanding more yield to absorb this massive new supply — and that premium is flowing into the long end of the curve. A second driver comes from the demand side. Historically, foreign central banks — particularly in Asia — absorbed enormous quantities of long-dated U.S. Treasuries as part of their foreign exchange reserves, which acted as a structural buyer that suppressed long yields. This demand is now declining as de-dollarization shifts reserve allocations toward gold and non-dollar assets. According to the Federal Reserve's own data, foreign official holdings of U.S. Treasuries fell by $128 billion over the past 12 months — the largest annual decline on record. Less demand from the traditional buyers means the Treasury must attract other buyers by offering higher yields.

왜 지금 장기 수익률이 오르고 있을까요? 핵심 개념은 기간 프리미엄(term premium)입니다 — 투자자들이 듀레이션 리스크(duration risk)를 감수하는 대가로 요구하는 추가 수익률입니다. 듀레이션 리스크는 장기간 채권을 보유하기로 약속하는 위험으로, 그 기간 동안 많은 일이 잘못될 수 있습니다. 인플레이션이 상승할 수도 있고, 정부가 더 큰 적자를 낼 수도 있으며, 달러가 더 약해질 수도 있습니다. 기간 프리미엄은 본질적으로 장기 불확실성에 대한 시장의 보험료입니다. 2010–2021년의 대부분 동안, 연방준비제도의 대규모 채권 매입 프로그램 — 양적완화(quantitative easing) — 는 장기 국채를 대량으로 시장에서 제거함으로써 기간 프리미엄을 인위적으로 억제했습니다. 양적완화가 끝나고 Fed가 이제 대차대조표를 축소하는 양적긴축(quantitative tightening)을 시행하면서 그 억제가 해제됐습니다. 더 직접적인 원인은 미국 정부의 재정적자(fiscal deficit) — 정부 지출과 세금 수입의 차이 — 와 그 적자를 메우기 위해 필요한 막대한 양의 신규 국채 발행입니다. 2026년 미국 재정적자는 GDP의 7.2%에 달하고 있습니다. 이 격차를 메우기 위해 재무부는 올해 순 신규 채권을 약 2조 1,000억 달러 규모로 발행해야 합니다. 이는 채권 공급의 엄청난 증가입니다. 기본적인 수요-공급 법칙: 공급이 늘어나는데 수요가 일정하면 가격이 하락합니다. 채권에서는 가격 하락이 수익률 상승을 의미합니다. 시장은 이 거대한 신규 공급을 소화하기 위해 더 높은 수익률을 요구하고 있으며, 그 프리미엄이 수익률 곡선의 장기 끝으로 흘러들어가고 있습니다. 두 번째 원인은 수요 측면에서 옵니다. 역사적으로 외국 중앙은행들 — 특히 아시아 — 은 외환보유고(foreign exchange reserves)의 일부로 장기 미국 국채를 대량으로 흡수했으며, 이는 장기 수익률을 억제하는 구조적 매수 세력으로 작용했습니다. 이제 탈달러화가 외환보유고 배분을 금과 비달러 자산으로 이동시키면서 이 수요가 감소하고 있습니다. 연방준비제도 자체 데이터에 따르면, 외국 공식 보유 미국 국채는 지난 12개월 동안 1,280억 달러 감소했습니다 — 사상 최대 연간 감소폭입니다. 전통적인 매수자들의 수요 감소는 재무부가 더 높은 수익률을 제공해 다른 매수자들을 유치해야 한다는 것을 의미합니다.

Ripple Effects: Mortgages, Stocks, and Businesses

Why does a bear steepener matter beyond bond markets? The 10-year and 30-year Treasury yields are the benchmark rates that directly influence borrowing costs across the economy. In the United States, the average 30-year fixed mortgage rate is typically priced at approximately 170 basis points above the 10-year Treasury yield. If the 10-year yield rises from 4.45% toward 5%, the average mortgage rate moves from approximately 6.15% toward 6.7% — a meaningful increase in the monthly payment for a home purchase. Corporate bonds are priced at spreads above Treasuries as well, meaning higher Treasury yields raise borrowing costs for businesses even before any change in credit risk. Rising long-term rates also compress equity valuations through a mechanism called discounted cash flow. The logic: when you buy a stock, you are buying the right to all the company's future earnings — stretching years or decades into the future. To determine what those future earnings are worth today, analysts use a discount rate — essentially the return they require for waiting. When long-term risk-free rates (Treasury yields) rise, the discount rate rises too, which mathematically reduces the present value of all future cash flows. Growth stocks — whose value is concentrated far in the future — are most sensitive to this effect. A 50 basis point rise in the 10-year yield is estimated to reduce S&P 500 fair value by approximately 7–10% through this channel alone.

베어 스티프너가 채권시장을 넘어 왜 중요할까요? 10년물과 30년물 국채 수익률은 경제 전반의 차입 비용에 직접적인 영향을 미치는 기준금리(benchmark rates)입니다. 미국에서 평균 30년 고정 모기지 금리는 일반적으로 10년물 국채 수익률보다 약 170베이시스 포인트 높게 책정됩니다. 10년물 수익률이 4.45%에서 5%로 상승하면, 평균 모기지 금리는 약 6.15%에서 6.7%로 오릅니다 — 주택 구매 월 상환액의 의미 있는 증가입니다. 회사채도 국채 대비 스프레드로 가격이 책정되기 때문에, 신용위험 변화가 없더라도 국채 수익률 상승은 기업의 차입 비용을 높입니다. 장기금리 상승은 또한 할인된 현금흐름이라는 메커니즘을 통해 주식 가치평가(equity valuations)를 압축합니다. 논리는 이렇습니다. 주식을 매수할 때, 여러분은 회사의 모든 미래 이익에 대한 권리를 사는 것입니다 — 수년 또는 수십 년 미래까지 뻗어 있습니다. 그 미래 이익이 오늘날 얼마의 가치인지 결정하기 위해, 분석가들은 할인율(discount rate) — 본질적으로 기다리는 것에 대해 요구하는 수익률 — 을 사용합니다. 장기 무위험 금리(국채 수익률)가 오르면, 할인율도 상승하여 모든 미래 현금흐름의 현재가치를 수학적으로 감소시킵니다. 가치가 먼 미래에 집중된 성장주들이 이 효과에 가장 민감합니다. 10년물 수익률이 50베이시스 포인트 상승하면 이 채널만으로도 S&P 500 적정가치를 약 7–10% 낮추는 것으로 추정됩니다.

What It Means for Korea

For Korean readers, there is an additional layer. The Bank of Korea holds approximately $410 billion in foreign exchange reserves, with a large proportion invested in U.S. Treasuries — particularly longer-dated maturities. When Treasury yields rise, existing bond prices fall, creating a mark-to-market loss on those holdings. At the same time, if the Bank of Korea reinvests maturing bonds at higher yields, future income from reserves increases. The net effect on Korea's external financial position depends on the pace and magnitude of the yield rise, but the short-term impact is negative: the dollar value of Korea's Treasury portfolio shrinks even as the bonds deliver higher ongoing income. What does this mean for South Korean exporters? The Korean won has strengthened to approximately 1,335 per dollar, itself partly a reflection of the dollar weakness that accompanies the bear steepener dynamic. Samsung Electronics and Hyundai Motor have both guided that each 1% won appreciation reduces annual operating profit by approximately 150–200 billion won ($112–$150 million). The interaction between U.S. long rates, dollar weakness, and won strength creates a complex environment for Korean exporters: they benefit from lower raw material input costs in won terms, but face headwinds on overseas revenue translation and competitiveness versus Japanese and Chinese rivals whose currencies have also strengthened. For Korean institutional investors — who hold significant allocations to US fixed income through pension funds and insurance companies — the bear steepener creates a mark-to-market loss on existing positions while simultaneously raising yields on newly purchased securities, requiring careful duration management to avoid realizing losses before reinvestment becomes accretive.

한국 독자들에게는 추가적인 맥락이 있습니다. 한국은행은 약 4,100억 달러의 외환보유고를 보유하고 있으며, 상당 부분이 미국 국채 — 특히 장기물 — 에 투자되어 있습니다. 국채 수익률이 오르면 기존 채권 가격이 하락하여 보유분에 대한 시가평가 손실이 발생합니다. 동시에, 한국은행이 만기 채권을 더 높은 수익률로 재투자하면 외환보유고에서 발생하는 미래 수입이 증가합니다. 한국의 대외 재무 상태에 대한 순 효과는 수익률 상승 속도와 폭에 따라 다르지만, 단기적 영향은 부정적입니다. 채권이 더 높은 지속적 수입을 제공하는 동시에, 한국의 국채 포트폴리오의 달러 가치가 축소됩니다. 이것이 한국 수출기업들에게는 무엇을 의미할까요? 한국 원화는 달러당 약 1,335원으로 강세를 보이고 있으며, 이는 베어 스티프너 역학에 수반되는 달러 약세를 부분적으로 반영합니다. 삼성전자와 현대자동차 모두 원화가 1% 절상될 때마다 연간 영업이익이 약 1,500억–2,000억 원(1억1,200만–1억5,000만 달러) 감소한다고 가이던스를 제시했습니다. 미국 장기금리, 달러 약세, 원화 강세의 상호작용은 한국 수출기업들에게 복잡한 환경을 만들어냅니다. 원화 기준으로 원자재 투입 비용이 낮아지는 혜택이 있지만, 해외 수익 환산과 역시 통화가 강세를 보이는 일본·중국 경쟁사들과의 경쟁력 면에서 역풍을 맞습니다. 미국 고정 수익에 상당한 비중을 투자한 한국 연기금과 보험사 등 기관 투자자들에게 베어 스티프너는 기존 포지션에 시가 평가 손실을 발생시키는 동시에 새로 매입하는 채권의 수익률을 높여요. 더 높은 금리로의 재투자가 누적적 효과를 내기 전에 손실이 실현되지 않도록 신중한 듀레이션 관리가 필요한 상황이에요.

What to watch

For individual investors navigating a bear steepener environment, the key principle is duration management. Duration is a measure of a bond's sensitivity to interest rate changes — roughly, how many years of cash flows are at risk. A 30-year bond has very high duration (around 18); a 2-year bond has low duration (around 1.9). In a rising long-rate environment, holding long-duration bonds causes losses, while short-duration bonds are relatively protected. This is why many fixed-income investors have been rotating from long-duration Treasury ETFs into short-duration instruments — Treasury bills, short-term bond funds, or money market funds — to reduce exposure to the term premium repricing now underway. Watch for whether the 30-year Treasury yield crosses 5.5% in the coming weeks — that level historically marks the threshold where pension funds and insurers are forced to rebalance away from equities, and a coordinated shift of that scale would reprice every risk asset in your portfolio simultaneously.

베어 스티프너 환경을 헤쳐나가는 개인 투자자들에게 핵심 원칙은 듀레이션 관리(duration management)입니다. 듀레이션은 채권의 금리 변화 민감도를 측정하는 지표입니다 — 대략, 얼마나 많은 연수의 현금흐름이 위험에 처해 있는지입니다. 30년 채권은 매우 높은 듀레이션(약 18)을 가지며, 2년 채권은 낮은 듀레이션(약 1.9)을 가집니다. 장기금리 상승 환경에서 장기 듀레이션 채권을 보유하면 손실이 발생하는 반면, 단기 듀레이션 채권은 상대적으로 보호됩니다. 이것이 많은 채권 투자자들이 장기 국채 ETF에서 단기 상품 — 국채증권, 단기 채권 펀드, 또는 머니마켓 펀드 — 으로 교체하고 있는 이유입니다. 현재 진행 중인 기간 프리미엄 재조정에 대한 노출을 줄이기 위해서입니다. 앞으로 몇 주간 30년물 미 국채 금리가 5.5%를 돌파하는지 주시하세요. 그 수준은 역사적으로 연기금과 보험사들이 주식에서 벗어나 재조정을 강요받는 임계점이에요. 그 규모의 조율된 이동이 일어난다면, 여러분의 포트폴리오 내 모든 위험 자산이 동시에 재평가될 거예요.